by admin | Dec 3, 2015 | Blog, Flood, FYI, Natural Disasters, Weather

Flood Insurance and Sewer Backup Insurance – Not the same thing. Floods are the most devastating natural disaster in the United States each year causing billions in losses and displacing thousands. While flooding is a common concern for those near rivers and streams,...

by admin | May 28, 2015 | Blog, Insurance

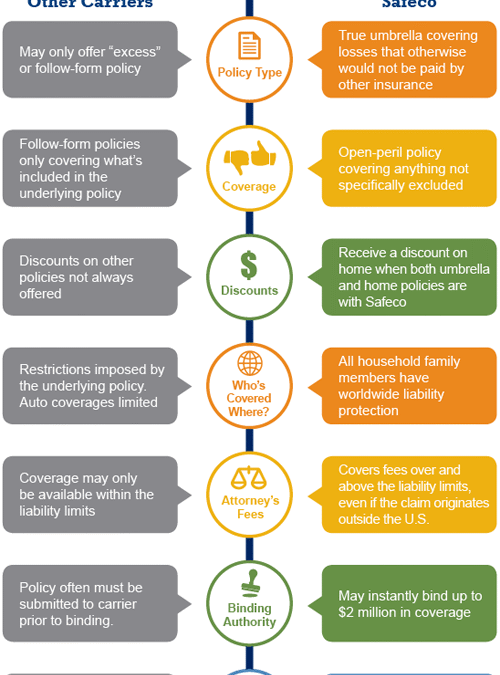

Is it worth it to buy an umbrella policy these days?

by admin | Apr 21, 2015 | Blog, Insurance

Just like hamburgers and hot dogs, a sizzling grill is a symbol of summer and grilling isn’t just about great food. Backyard barbecues often create treasured memories with friends and family. Keep in mind, however, that when you grill, you’re literally playing...

by admin | Feb 25, 2015 | Blog, Insurance

It’s exciting to receive jewelry from a loved one — or to give it as a gift. Not to mention romantic. But if you’re lucky enough to have some new jewelry in your home from Valentine’s Day, you should take a few minutes to think about something you...

by admin | Jan 20, 2015 | Blog, Insurance

This is a great optional coverage for a nominal price that can be added to your homeowner’s policy. With all the social media craze these days it would be wise to make that extra step to cover you while you are on Facebook, Twitter and the like. Here is an...

by admin | Dec 16, 2014 | Blog, Insurance

You know it’s here. Snow and slush. Freezing rain. Maybe even black ice. But do you know if your tires are ready for all of that? When driving in St. Louis Mo in the wintertime, your tires just might be the most important safety feature on your car. The right ones can...